Our Web3 Future

BY KEITH TEARE • ISSUE #296 • VIEW ONLINE

Web3 is becoming a more familiar label for innovative technologies. But what is it? This week Maggie Hsu from Andreessen Horowitz gets the lead position for her article covering what makes Web3 marketing different.

Contents

Editorial

Tech stocks have somewhat rebounded this week so it has been possible to forget how much value has disappeared from the public markets. And while there are some interesting developments in the venture capital space (Tiger Global’s new $11bn sidecar fund, a great profile of Roelof Botha and Blackrock predicting 1000 energy sector unicorns) other things caught my attention.

Jessica Lessin’s wonderful writing covering the Facebook, Google, Apple universe was one. MG Siegler’s piece is a nice complement. Foundry Group terminating its two SPACs is another. The SPAC world has really ceased to be a viable path to a public offering for most companies. Forbes, with $200m from Binance newly banked, seems an unlikely candidate for example.

But top of the list for an attention-grabbing read was Andreessen Horowitz partner Maggie Hsu’s piece on Future covering the differences in go-to-market strategies between Web3 companies and their Web2 predecessors. It is a long thoughtful piece by an experienced product marketer. It really helps somebody contemplating a Web3 product understand the key elements of success and chart a path to navigating their journey. She ends with the following summary:

The key difference to remember is that the goals, growth, and success metrics of web2 and web3 are often not the same. Builders should start with a clear purpose, grow a community around that purpose, and match their growth strategies and community incentives — and with them, the go-to-market motions — accordingly.

The building blocks to arriving at that summary are a must-read. Hsu starts out stating:

This new model, known as web3, changes the entire idea of GTM for these new kinds of companies. While some traditional customer acquisition frameworks are still relevant, the introduction of tokens and novel organizational structures such as decentralized autonomous organizations (DAOs) requires a variety of go-to-market approaches.

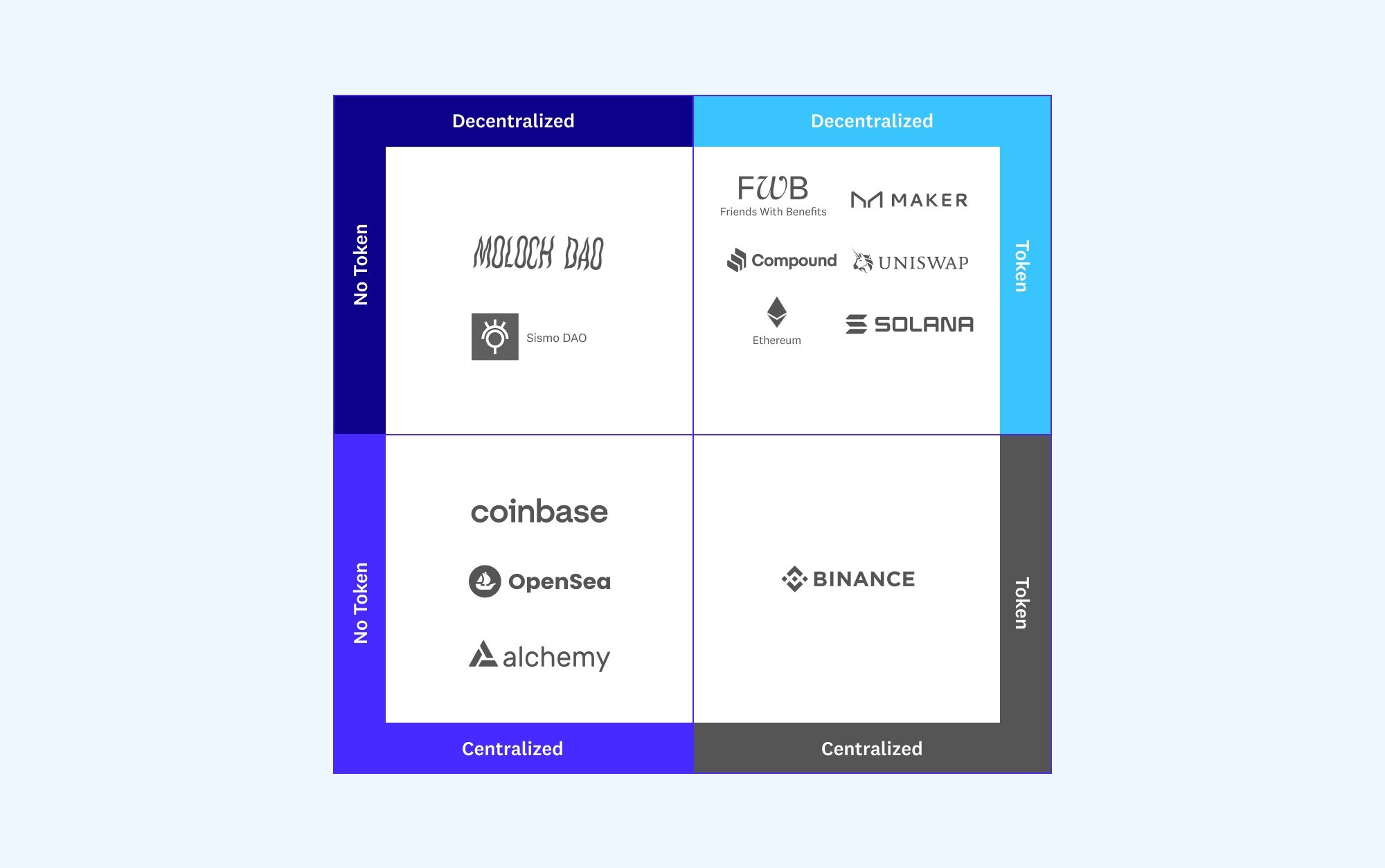

It goes on to look at the difference in go-to-market strategies available to differing types of organizations as depicted in this matrix:

Hsu drills down into the differing organization types, with and without tokens, and suggests ways of thinking about successful market entry.

Honestly, I have nothing to add to her work other than to suggest you read it. Even if you are not a Web3 participant it will clarify much about what characterizes Web3 and why it is part of our future.